Cash Credit Limit: Lifeline or Liability?

Devesh Srivastava, Advocate

Associate Member, JTS Lex.

(Author’s outlook)

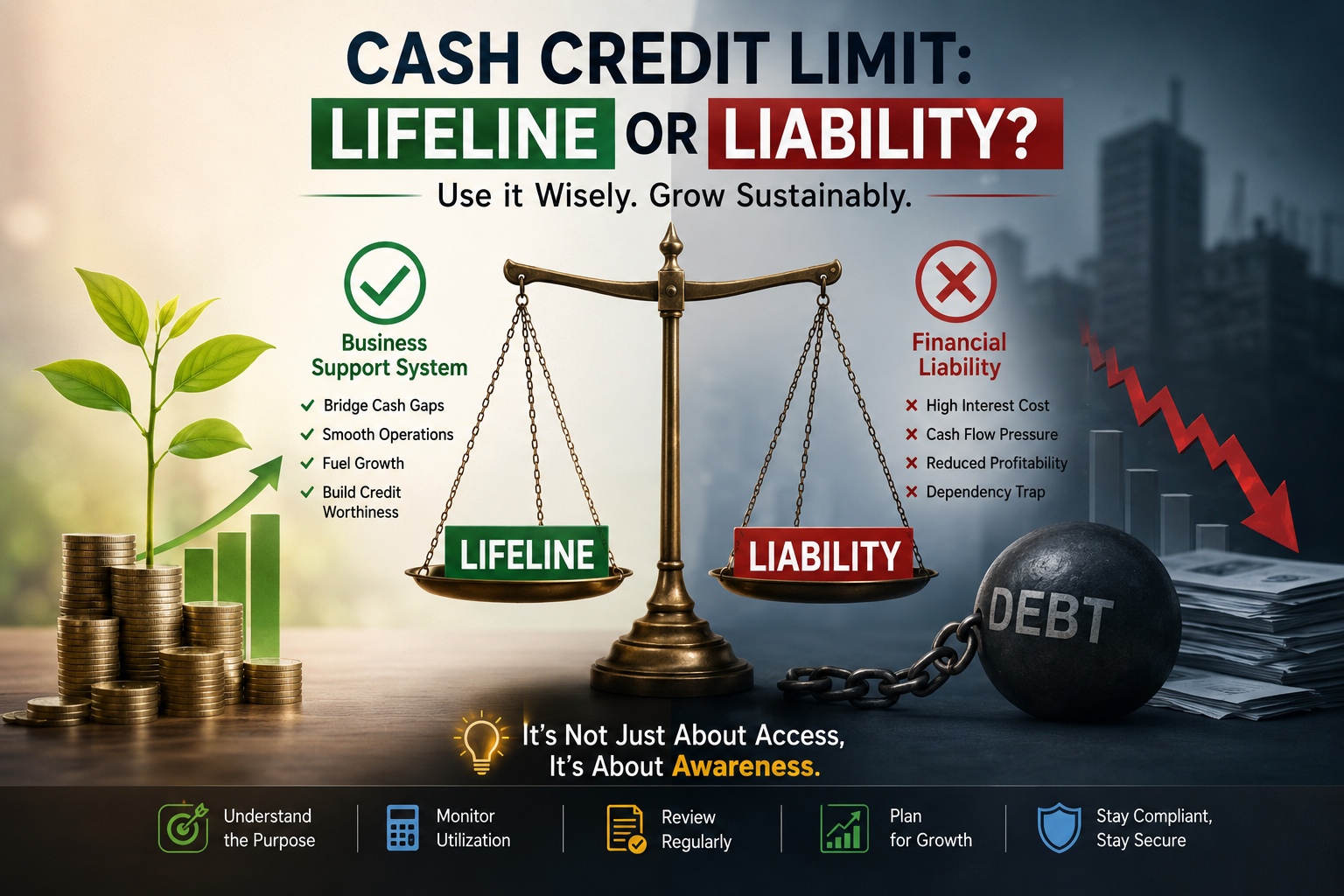

On financial and legal scrutiny, it is often observed that businesspersons initially treat a Cash Credit (CC) limit as a facility of convenience. However, over time, this perceived convenience evolves into dependency, and eventually into a structural compulsion that may adversely impact on the financial health of the enterprise.

A dispassionate and analytical understanding of the mechanism is therefore essential:

1. It Is Not Your Capital, But Borrowed Liability

A fundamental misconception among borrowers is treating CC funds as their own working capital. Such funds are extended at a cost, namely, interest, which steadily erodes profit margins. For instance, a CC limit of ₹1 crore, if consistently utilized to its full extent, may result in an annual interest outflow of approximately ₹10 to 12 lakhs. This effectively implies that a substantial portion of the business effort is directed towards servicing the bank’s interest rather than generating net gains.

2. Intended as a Revolving Facility, not a Long-Term Borrowing Instrument

Legally and commercially, a CC facility is structured as a short term, revolving line of credit intended to bridge temporary working capital gaps. The underlying principle is cyclical usage: funds are withdrawn for inventory or operational needs and repaid upon realization of receivables. However, in practice, many enterprises utilize CC limits akin to term loans, thereby incurring higher interest costs without structured repayment discipline.

3. Enhancement of Limit: Growth Indicator or Debt Accumulation?

An increase in CC limit is often misconstrued as a sign of business growth or financial credibility. From a legal-financial perspective, it simultaneously signifies increased exposure and liability. If, over an extended period, the business remains reliant on bank borrowing for sustenance rather than growth, it raises serious concerns regarding the viability and efficiency of the underlying business model.

4. The Compounding Effect of Daily Interest Calculation

CC facilities typically operate on a daily interest calculation basis. This imposes a continuous financial burden, making prudent fund management imperative. Failure to deposit surplus funds into the CC account while maintaining negative balances and simultaneously holding idle funds in savings accounts reflects inefficient financial planning and results in avoidable interest costs.

A Cash Credit facility ought to be treated as a contingent financial buffer a safety net, rather than an essential life support mechanism. As a matter of sound financial discipline, it is advisable that the CC account periodically reflects a nil or credit balance, ideally at least twice within a financial year. Persistent overutilization is indicative of systemic inefficiencies and potential financial distress.

It must be borne in mind that institutional finance is intended to augment business velocity, not to artificially sustain its existence.

In conclusion, prudent financial management demands that one strengthen the balance sheet of the enterprise not that of the lending institution.